Your credit score is an important measure of your creditworthiness and impacts your insurance and borrowing costs.

Even established investors should be cognizant about having a strong credit score because it can impact the premiums you pay for insurance and the rate of interest you pay on loans. You might want to open a new credit card to receive a bonus for signing up, but opening and closing credit card accounts can reduce your credit score. The question is, just how much does it impact your credit score, and is it worth sweating?

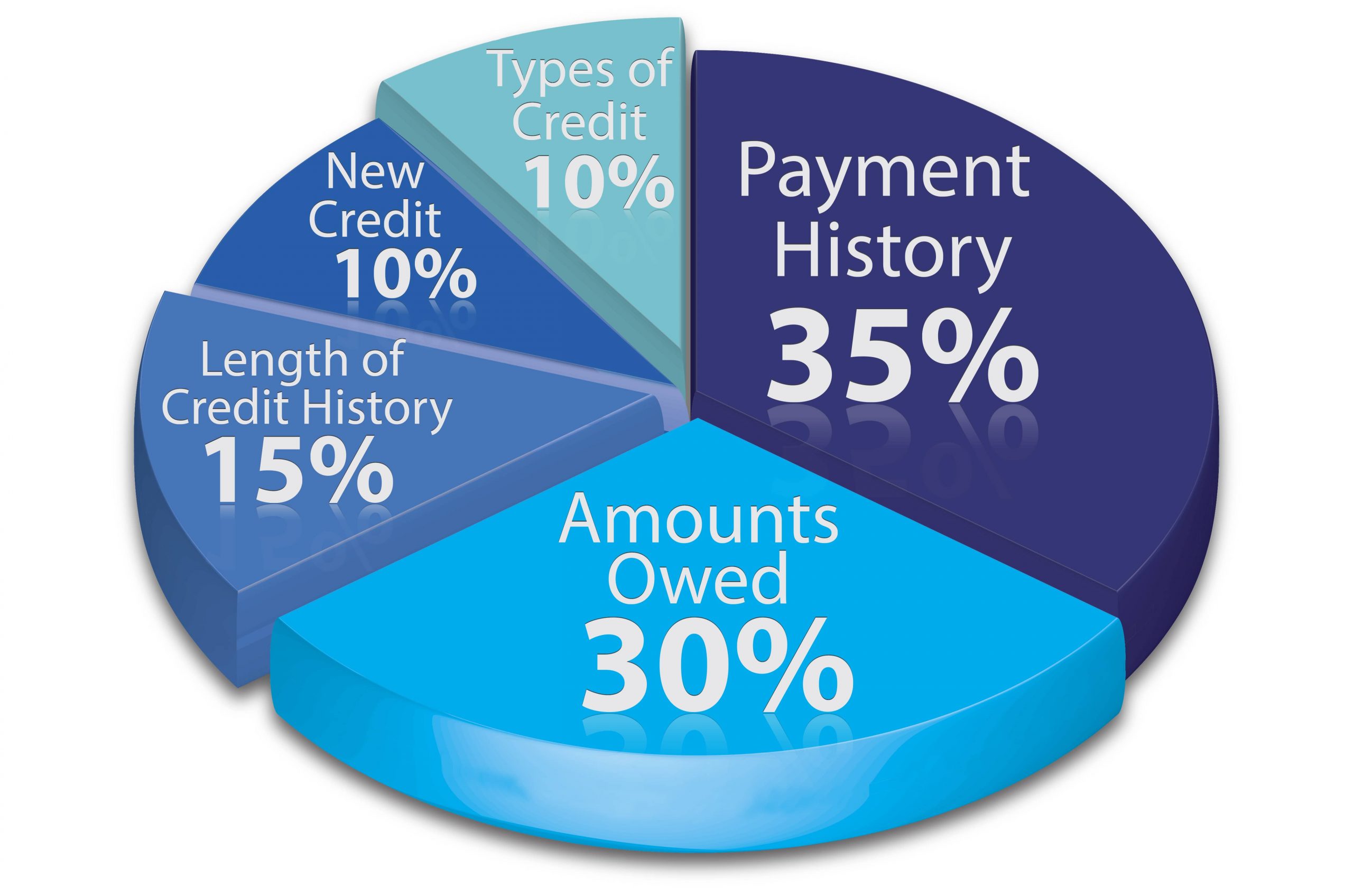

Most banks and credit lenders use FICO, which is the most common type of credit score. FICO scores range from 300 to 850. The score is based on the credit files of the three national bureaus – Experian, Equifax and TransUnion – with the following breakdown:

- Payment history 35%fico image

- Amounts owed 30%

- Length of credit history 15%

- New accounts 10%

- Types of credit used 10%

An overview of your credit component breakdown

Your Payment history (35%) is how well you demonstrate the ability to make payments on time. Even if you cancel a credit card, the payment history on that card will stay on your credit report for 10 years after the day it was closed.

If you’re just making minimum payments, you are paying the contractual minimum so that alone doesn’t hurt your credit score. Adding an automatic deduction for the minimum payment or calendar reminders is a great way to never forget or make a late payment.

Amounts owed (30%) measures how much you’ve charged in relation to your overall available credit. This can also be called your “credit utilization rate”, and keeping it lower than 20% of overall limit is ideal. Credit bureaus use three other metrics in addition to the credit utilization rate, including the number of accounts with balances, the amount owed across different types of accounts and the amount paid down on installment loans.

Canceling a credit card that has a high limit can hurt your credit score because it impacts your utilization rate. Be careful not to close credit cards before a big purchase like a home or a car, because you want your credit score to be as high as possible to get the most favorable interest rate and terms available. Having a credit utilization rate of over 30% can hurt your credit score.

The Length of history (15%) component has a positive impact on your credit score. The two metrics tracked include average age of accounts and the age of your oldest account. It can be said that the oldest credit cards are the best credit cards for your credit score. This also takes into account how long other types of credit (auto, student, mortgage, etc.) have been established.

Closing a credit card may reduce the average age of accounts. Opening a new credit card will also reduce your average age of accounts, which hurts your score. The ideal age of credit card accounts is eight years or older.

New credit (10%). Recent searches (also called hard inquiries) into your credit history, such as when you apply for a new credit card, can hurt your credit score. Hard inquiries also occur when a lender is evaluating other types of loans (e.g. auto, home or business loans). A soft inquiry, which occurs when opening a new brokerage account or part of a new employer’s background check, does not impact your credit score.

Having a mix of different types of credit (10%) helps your score. Types includes installment (auto loan), revolving (credit card), consumer finance (high interest rate, short-term loans like from Payday loans) and mortgages.

For those of you interested in an estimate of your FICO score, you might consider trying to us the online credit score estimator.