Blog Subscription

To subscribe to our blog, simply fill out the form below.

To subscribe to our blog, simply fill out the form below.

The Year in Review – Prognosticators Anticipated the Worst, While the Markets Advanced to All-Time Highs

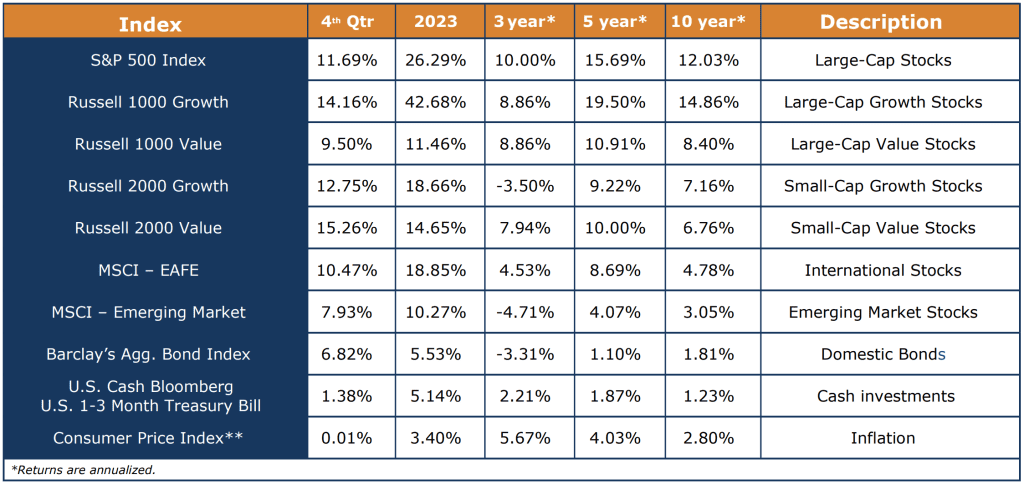

At the beginning of 2023, consensus expectations for economic growth and stock market returns were negative. The “talking heads” in the media, authors of financial newsletters, and even many well-renowned economists believed that the Federal Reserve would raise rates too quickly to bring down inflation, which had spiked at 9.1%. The threat of recession drove many fearful investors to move funds into money markets and other cash investments. Making cash further tempting was that interest rates had risen to about 5%, levels not seen since prior to the Great Recession of 2008. However, making rash decisions and missing out on strong returns can be hazardous. It is another reminder of how being on the sidelines and trying to time the market is unlikely to provide better results than staying the course. All equity markets were in double-digit territory in 2023 as shown below:

To offer a sense of just how impressive the returns were for the US market, the S&P 500 Index performance was twice that of the long-term average. Since the inception of the Index in 1957, the S&P 500 has generated an average annual return of +12.1%. In 2023, it was up an astounding +26.29%!

Also of interest are the comparisons of growth versus value stocks within the large-cap areas. Although large-cap growth received much of the media attention in 2023 due to its outsized returns (+42.68%), it also declined the most in 2022 (-29.14%). Large cap value stocks rose less (+11.46%) in 2023, but also declined much less (-7.54%) the previous year. If you compare the two asset classes over a three-year period from 2021-2023, the end results were actually identical at +8.86%, but they took two very different paths to get there. The benefit of holding both (along with all the asset classes in a portfolio) is that through rebalancing, more shares are bought while one asset class is down and other shares are sold while at a relative high point. The cardinal rule of buying low and selling high is achieved and results in added growth to the portfolio!

For mid- and small- capitalization stocks, as illustrated with the Russell 2000 Indices, growth outperformed value in 2023, up +18.66 and +14.65%, respectively. However, they performed somewhat differently over a 3-year cycle. The Russell 2000 Value generated an average annual return of +7.94% while Russell 2000 Growth declined -3.50%.

International markets increased dramatically during the period as well, as measured by the MSCI –EAFE Index, which advanced +18.85%. Emerging markets grew a little more modestly, increasing +10.27% for the year as measured by the MSCI – Emerging Markets Index.

Lastly, relative to the bond market, most investors are painfully aware that in 2022 bonds had their worst performance in over 50 years. Due to dramatic increases in interest rates, the bond market dropped -13.01%, as measured by the Barclay’s Aggregate Bond Index. In 2023, the bond market began to stabilize, and the overall return was +5.14%.

2024 Outlook – Election Season is Likely to Create Short-term Market Volatility

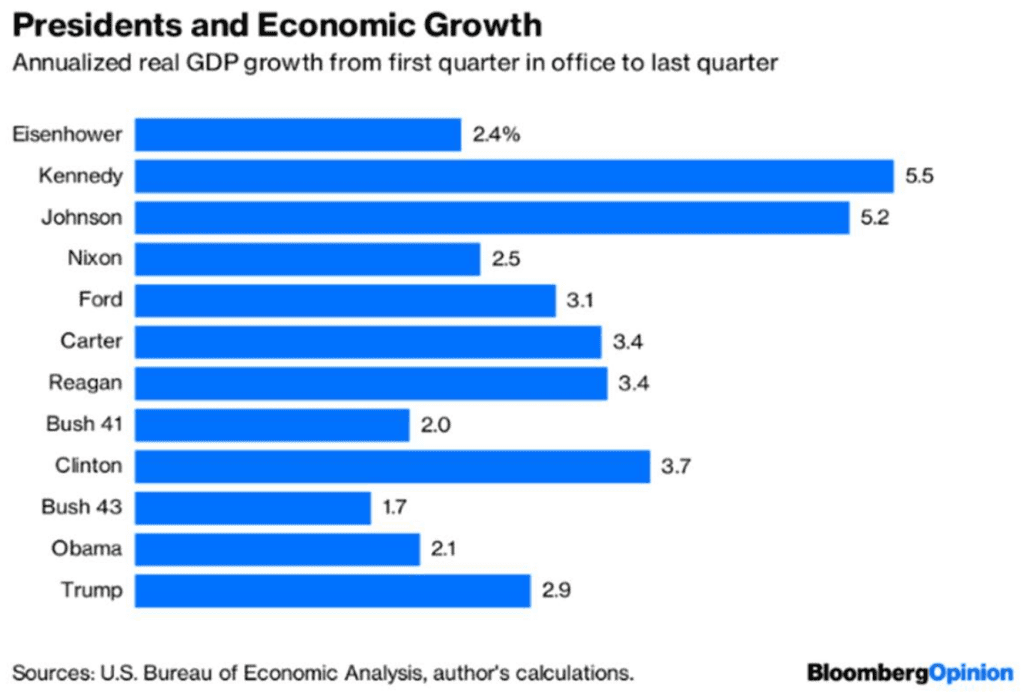

As the year begins, news about the Presidential Election is already dominating the headlines. Just like in 2023, however, it is important to avoid reactive investment decisions based upon political events, which may change daily. No matter which side of the aisle you are on, you have probably read or heard some of the lurid doomsday predictions made by the very same pundits that erroneously predicted a recession in 2023. Sadly, these wildly inaccurate prognosticators spew the same hyperbole during every presidential election year. Depending on who is in office, they say, the market will either plummet or skyrocket. The reality, however, is that market performance is not affected by who wins the election. Instead, the direction of the markets is driven by the general state of the economy and corporate profits, which in turn are driven by a host of factors such as unemployment rates, inflation, interest rates, manufacturing and inventory levels, oil prices, consumer spending, etc.

In truth, the economy has grown under each President since the Eisenhower administration as illustrated in the chart below:

In addition to the economy, the stock markets also advanced during each of these Presidential terms with two notable exceptions: Richard Nixon and George W. Bush (#43). In the case of Nixon, there was rampant inflation for several years along with skyrocketing oil prices, which negatively impacted corporate profits. Even then, the markets would have recovered during his tenure, had it not been cut short due to the Watergate scandal. George W. Bush’s term began after a period when technology stocks had experienced outsized investment returns, which was a result of several years’ worth of unrealistic growth expectations. The subsequent decline happened to correspond with the beginning of his time in office. The sizable drop in the markets, now referred to as the “tech wreck”, proved too much to recover from before the end of his Presidency.

Prudent Portfolio Management Integrated with Comprehensive Financial Planning Provides the Best Long-Term Results

Many people become fearful during ominous economic and investment times, which often cause them to behave inappropriately as investors. Fear drives investors to run away when they likely should be moving forward, and immobilized when they should be taking informed, positive actions. When consumer sentiment is low and news relative to world events is unsettling, equity markets most often bounce back.

Rather than being reactionary to daily news commentaries, we steadfastly remain emotionally detached from the day-to-day, and advocate a proven Nobel Prize-Winning Approach for managing our clients’ investment portfolios. By maintaining a consistent exposure to a diversified array of asset classes, and making tactical shifts over and above periodic rebalancing and profit taking opportunities, we seek to add value to our client portfolios, especially during periods of elevated volatility. Also, by continuously monitoring for tax loss harvesting opportunities in taxable porƞolios, our clients benefit from a lesser tax burden and thereby increased investment returns.

At Total Wealth Planning, our team of financial planning and investment management professionals work closely together to ensure that opportunities for adding value to your financial situation are not overlooked. In our opinion, wealth-building and preservation must include not only investment management, but also financial planning activities. These include cash management, debt management, tax planning, risk management, college funding, retirement planning, and estate preservation.

We appreciate the trust and confidence clients have placed in us and we look forward to seeing you in 2024!