The human brain is not wired to be great at investing. The more investors who understand this, and can see how emotions and mental shortcuts are rooted in the following biases, the more successful an investment experience they can have.

Below are five behavioral biases…

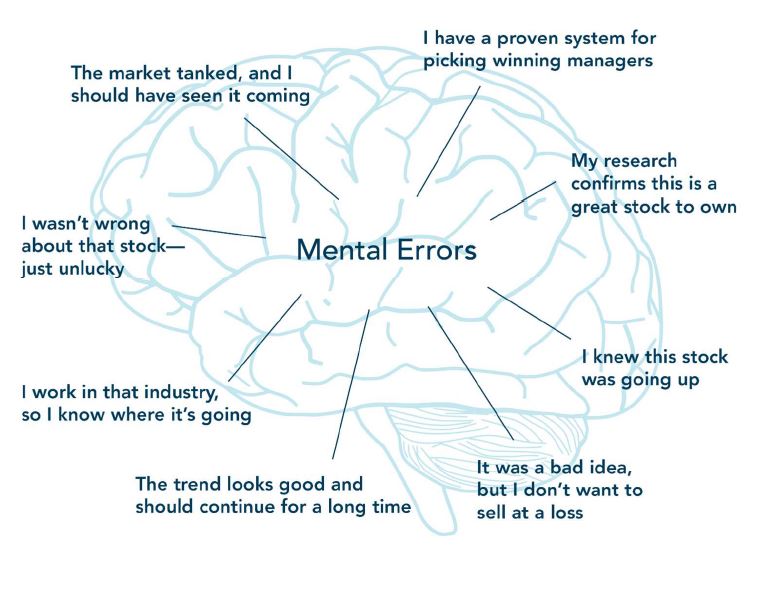

1. Outcome Bias

People often judge their decisions based on how they turn out, not how sound they were at the time. Say you invest in a long-term holding just before it starts to underperform some arbitrary market index. Does that make the decision a bad one? We hope not, but it might feel that way.

What you can do: It’s okay to indulge in the curiosity of comparing your investments with market indices, but it’s much more meaningful to focus on how you are progressing toward your market goals, longer term, instead of whether you are beating or lagging market indices.

2. Recency Bias

Say you flip a coin and get heads. Will the next flip be heads or tails? Our brains look for a pattern: The next flip will probably be tails, right? Or maybe heads is on a roll? (Fact: The odds are 50/50 no matter how many coins you flip.) This bias can lead an investor to assume an underperforming investment either will keep lagging or is due for a bounce.

What you can do: Understand that short-term returns are unpredictable and will not behave a certain way in response to past events.

3. Anchoring Bias

Our brains tend to get attached (or anchored) to a particular number. This bias can cause investors to behave irrationally. For example, if one reads a story about an investor who earned 12 percent annually, they might anchor on that number and expect unrealistic returns.

What you can do: Understand the actual past stock (and bond) market returns so you can have better expectations for what a diversified portfolio is capable of achieving based on the amount of bond and stock allocations, and also the variability during different economic cycles, inflationary pressures, and short-term versus long-term. Remember, stocks sometimes suffer steep losses, and if you are a net buyer of stocks on sale, your expected return is likely to increase.

4. Availability Bias

This is the tendency to make judgments based on the available pieces of information we think are most important – even if they’re not. This a huge problem in the era of 24/7 news cycles and no shortage of correct and inaccurate information on the internet and social media.

What you can do: A long term investor should “tune out the noise” and focus on what really matters to their families – their goals and the plans to reach them. Over time, you’ll find the “news da jour” does not and should not impact your future desires.

4. Hindsight Bias

You’ve heard the saying hindsight is 20/20. People often attempt to predict future outcomes even when it’s near impossible to be accurate. It’s a shortcut our brains use to deal with uncertainty. For example, if Outcome A happened in the past, then it should happen again in similar circumstances. I’m sure you have also heard “past performance doesn’t guarantee future results.”

What you can do: Be aware that decisions and outcomes are clear as day when looking in the rearview mirror. Many investors claim to have predicted past stock declines, after the fact. But in reality, few investors accurately predicted the bursting of the dot-com bubble in 2000, the magnitude of the 2008 decline, or the swift decline during the Coronavirus pandemic.

Disconnecting YOUR emotions from YOUR money decisions is always the best prescription

As an investor, you have an advantage by knowing these biases, but truly disconnecting YOUR emotions from YOUR money is a very difficult thing to do, especially during very scary or irrational exuberant times. As a holistic financial advisor, we partner, educate and guide clients through complex and difficult financial decisions every day. A fee-only wealth advisor can help keep your financial plan’s funding vehicle (i.e. your investments) on track when emotions may otherwise cause us to sell stocks at the worst time.