If you are like the many Americans who are looking for more opportunities for retirement savings, you may have come across the term “Backdoor Roth Contribution.” Your research may have prompted you with a plethora of unanswered questions about this strategy, such as: what is it, who is eligible, and perhaps most importantly how do you make sure this strategy is completed correctly? Each year, our team answers a variety of those questions, and provides clarification with this strategy. Unsure what a “Backdoor Roth IRA” is? Check out our Backdoor Roth explainer video HERE.

What is the Backdoor Roth IRA contribution strategy?

The Backdoor Roth IRA strategy is designed to give high-income earners the opportunity to invest in a tax-free Roth IRA. Growing your tax-free bucket can be an important component to saving for retirement, especially for younger investors, who can use many years of compound growth before withdrawing funds tax-free long into retirement. Whether to utilize this strategy varies but may be worthwhile if there is excess surplus after fully funding an emergency fund, and at least taking advantage of any employer retirement plan match contributions.

Who is eligible for a Backdoor Roth IRA contribution?

The Backdoor Roth strategy is most beneficial for those whose household income is above $240,000 (fully phased out from direct Roth IRA contributions), and specifically for those who do not have a pre-tax balance in a Traditional IRA. Making a non-deductible IRA contribution (subject to IRS limits) to a Traditional IRA has no income limitation as opposed to a deductible IRA contribution. The key distinction is that a non-deductible contribution can be converted to a Roth IRA tax-free since a non-deductible contribution is considered to be after-tax money. Therefore, an investor who has earned income above the Roth IRA contribution income limitation and no pre-tax funds in an IRA can use this strategy without any tax implications if reported correctly.

How should an investor make sure this strategy is completed correctly?

The first and obvious part of this strategy is following each step properly, which is illustrated in another Total Wealth Planning blog. Once that is done, a crucial step is accurately reporting this strategy on your tax return.

- Reporting your non-deductible IRA contribution: Since a contribution was made to an IRA, you will need to specify with the IRS that this was a non-deductible contribution by using IRS Form 8606. This form helps prevent paying unnecessary taxes on the Roth conversion since the IRS would otherwise assume that the amount converted was made with pre-tax dollars and be fully subject to taxation.

- Reporting your Roth conversion: Your custodian will generate Form 1099-R for your IRA reporting the Roth conversion. At face value, the 1099-R makes it look like you made a taxable IRA distribution. Therefore, it’s important to file Form 8606 to note that the amount converted was post-tax dollars, and therefore can be considered tax-free. If you convert any pre-tax dollars, or earnings in addition to your non-deductible IRA contribution, you still need to use Form 8606 to specify the taxable versus tax-free portion of the Roth IRA. It should also be noted that if two spouses each complete a Backdoor Roth contribution, separate 8606 forms are required to be filed with the tax return.

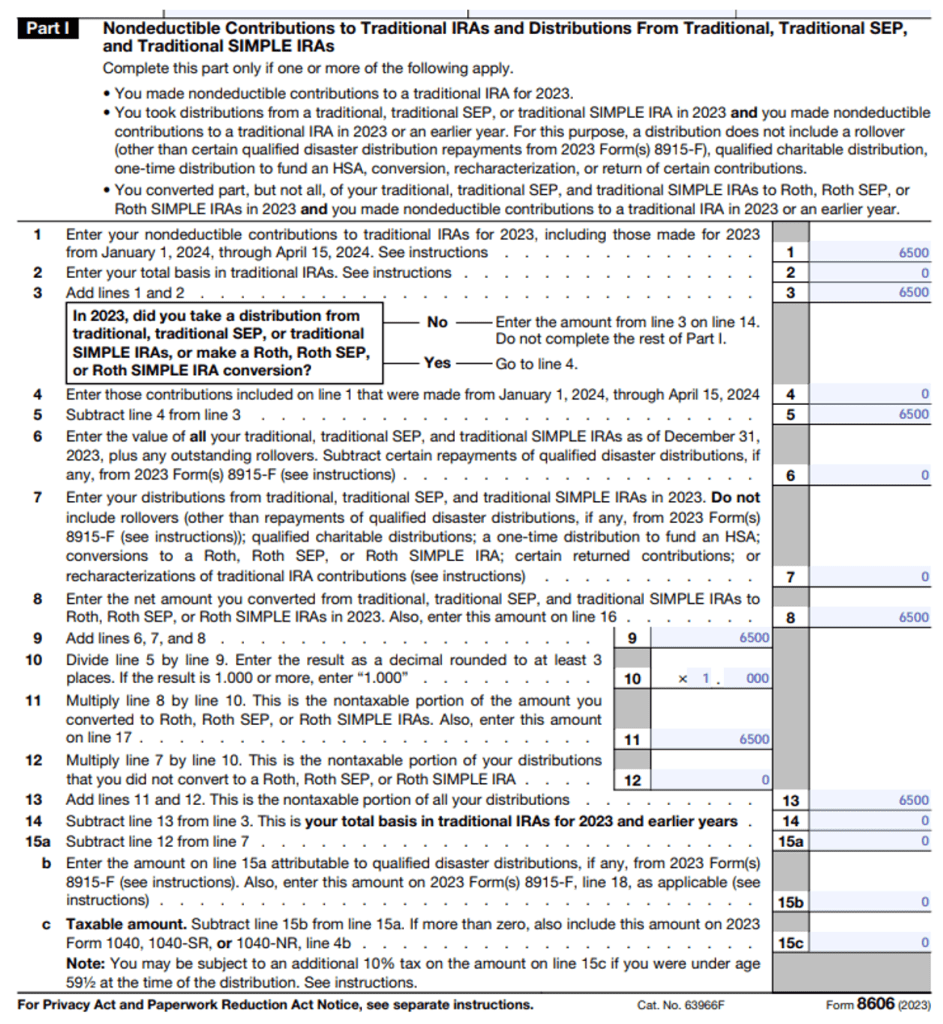

- Form 8606 Sample: To visualize how to report your Backdoor Roth contribution correctly, see below an example of an investor who completed this strategy in 2023 in the max amount eligible for individuals below 50 years of age ($6,500 in 2023). Page 1 of form 8606 is used to report the contribution.

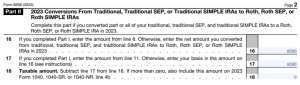

- On page 2, the investor will report the conversion and the taxable amount as seen in the example below.

Since there are potential tax consequences when doing this strategy, it is important to seek guidance from your tax advisor regarding this strategy.

About The Author: Holden Varvel is a licensed Financial Planner at Total Wealth Planning, a fee-only fiduciary financial planning firm in Cincinnati (Blue Ash), Ohio. “Golden Holden” serves as a Financial Planner for the firm and supports the financial planning team with insurance analysis, tax projections, college and retirement analysis, and other updates to client’s financial plans since he joined in late 2019. Holden also supports clients with various administrative tasks and problem solving to make client lives a little easier. Prior to joining the firm, Holden helped clients with tax, life insurance, payroll and bookkeeping solutions. Holden can be reached at holden@twpteam.com.