Our team was excited to see Professor Jeremy Siegel speak at Xavier University’s McCormick investment symposium late last month.

Jeremy Siegel is a well-respected professor of finance at the Wharton School of the University of Pennsylvania. After earning graduating from Columbia University in 1967, he earned his Ph.D in economics from MIT, with post-doctoral work at Harvard. He writes and lectures extensively about the economy and financial markets. Additionally, he is the author of “stocks for the long run” and recently, “Future for investors”.

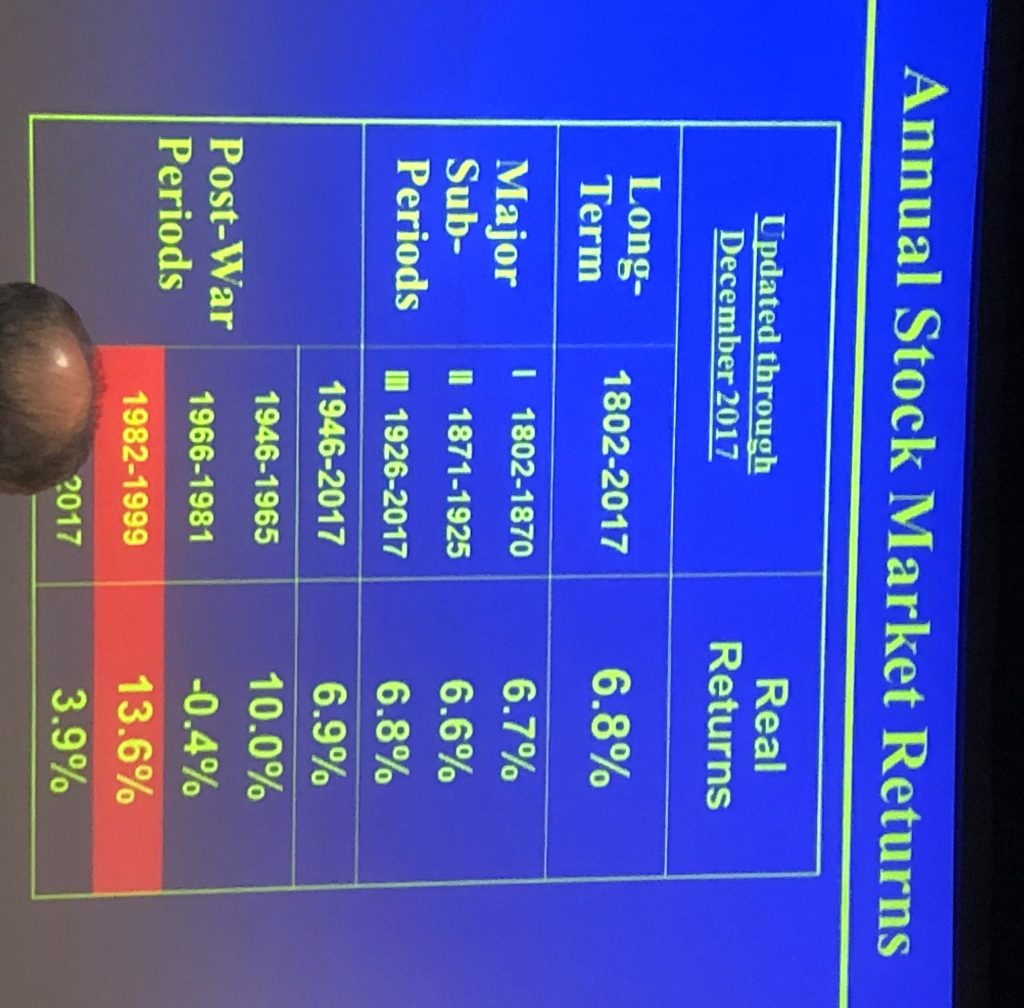

Considering the recent market volatility and the preceding 20 months of a soaring stock market, it was good to hear from such a distinguished finance academic. With much talk about market highs and comparing to the peak in 1999, he talked about some differences between then and now. The market peak of 1999 signaled the end of the world’s strongest bull market to date. That rocket ship took off in the early 1980’s and continued to fire its boosters all the way through 1999, returning 13.6% annually, after inflation (i.e. Real return) to those investors who got in and buckled up for the historic journey. As the slide shows below, those same markets have only rewarded investors with a 3.9% return over inflation since the previous peak.

Considering the recent market volatility and the preceding 20 months of a soaring stock market, it was good to hear from such a distinguished finance academic. With much talk about market highs and comparing to the peak in 1999, he talked about some differences between then and now. The market peak of 1999 signaled the end of the world’s strongest bull market to date. That rocket ship took off in the early 1980’s and continued to fire its boosters all the way through 1999, returning 13.6% annually, after inflation (i.e. Real return) to those investors who got in and buckled up for the historic journey. As the slide shows below, those same markets have only rewarded investors with a 3.9% return over inflation since the previous peak.

He further compared market expectations and valuation metrics in 1999 versus today. The market in 1999 had a P/E of 30 compared with 24 today. Looking closer, today’s market valuation is really at 20, but with some exciting tech stocks at 90 (e.g. FANG stocks). Another big difference with today’s tech stocks are the level of earnings and profits they’re reporting compared to mostly ideas and unproven revenue models of the late 90’s.

He explained a variety of ways to calculate and value earnings, such as GAAP, S&P operating, and firm reported. While there are pros and cons to each, he reassured the group that all methods of calculating earnings show optimism and growth ahead. Based on his method of forecasting expected returns, he forecasts stock returns after inflation (i.e. Real return), otherwise known as the equity risk premium. Today, he sees that expected risk premium at 4.5%. Compare this with 1999 when the expected market return was 3.3%, TIPS (i.e. inflation bonds) were paying 4.5%, and the risk premium was negative. In hindsight, investors were better off in US inflation treasuries than taking market risks. He used his valuation methodology across many countries and found healthy equity risk premiums no matter the country. In fact, he shared his 2018 outlook pointing towards more attractive valuations outside the US. Reflecting on client portfolios, we’ve started to see an uptick in foreign stock returns over their US counterparts.

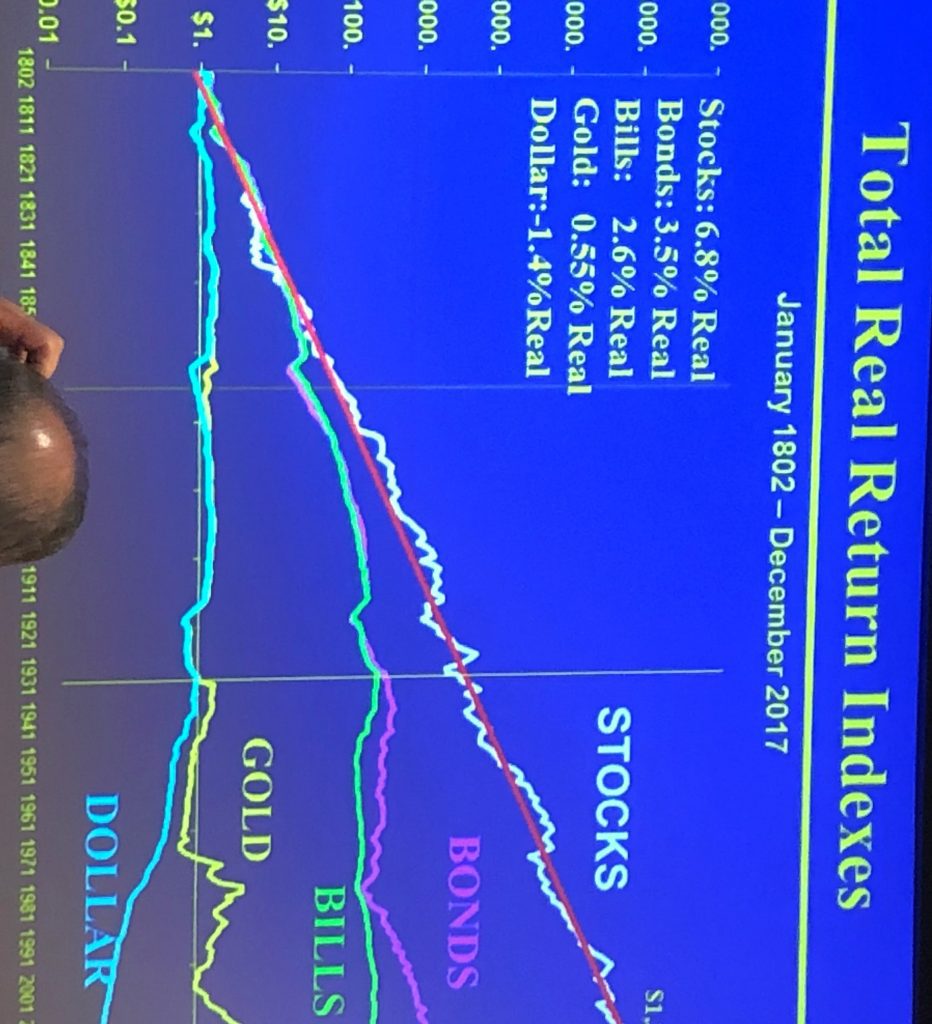

In the end, Professor Siegel and our team agreed that longer term, stocks will outperform all other investment options like cash and bonds as shown over the past 200 years. However, no one knows what will happen in the short term, but you shouldn’t invest in stocks unless your time horizon is 5 years or longer. Even though investors know this long term data, they continue to be scared of the short term volatility and the risk of total collapse. I like to believe the families who choose to partner with our firm are happier, less stressed, and are able to achieve their most important lifetime goals as a result of our coaching them through short term events so they can finish the marathon of managing their investment portfolio and constantly tweaking their Total Wealth Plan.

In the end, Professor Siegel and our team agreed that longer term, stocks will outperform all other investment options like cash and bonds as shown over the past 200 years. However, no one knows what will happen in the short term, but you shouldn’t invest in stocks unless your time horizon is 5 years or longer. Even though investors know this long term data, they continue to be scared of the short term volatility and the risk of total collapse. I like to believe the families who choose to partner with our firm are happier, less stressed, and are able to achieve their most important lifetime goals as a result of our coaching them through short term events so they can finish the marathon of managing their investment portfolio and constantly tweaking their Total Wealth Plan.

Total Wealth Planning LLC (“TWP”) is a registered investment advisor with the SEC. Past performance is no guarantee of future results. It is not possible to invest directly in an index.